A summary of the article “Dried Mango Prices Steady as Vietnam FOB Holds, Thailand Faces Heat and Storms” published on Commodity Board on 3 May, 2026

Market Stability Amid Environmental Challenges

The global dried mango market is currently characterized by a period of relative price stability despite emerging environmental risks in Southeast Asia. As of early May 2026, export offers from the primary producing regions—Vietnam and Thailand—have remained steady. While internal pressures like intense heat and seasonal storms are mounting, they have yet to trigger a significant “price shock” in the processed fruit segment, keeping short-term outlooks flat to slightly firm.

Vietnam: Steady FOB Prices and Harvest Support

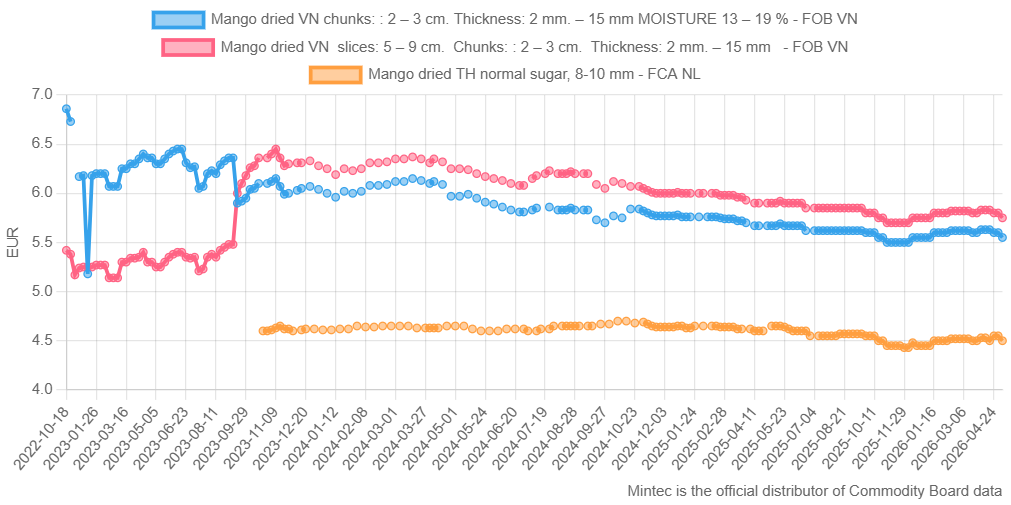

In Vietnam, Free on Board (FOB) prices out of Hanoi for conventional dried mango slices and chunks are holding firm at approximately 5.6 to 5.8 EUR/kg. This stability is largely attributed to the country entering its main harvest window (April–May), which ensures a consistent flow of raw material to processors. Despite a macro-forecast of hotter-than-normal temperatures and a delayed rainy season in southern regions, the ample supply from the current harvest has prevented any immediate downward pressure on prices.

Quality Concerns vs. Immediate Availability

A key distinction made in the market report is that current weather patterns—specifically extreme heat in Vietnam and storms in Thailand—are primarily impacting fruit quality and processing yields rather than total volume availability. This means that while standard stock remains available, there is a growing risk of shortages in “high-spec” or premium grades. Traders are being advised to monitor these quality-related signals, as they could lead to a price premium for top-tier products later in the season.

Global Demand and Diversification Trends

Demand for dried mango in the European and Asian markets remains robust, driven by a desire to diversify supply chains away from single-origin risks. Both Thailand and Vietnam are benefiting from this trend, especially as logistics risks and seasonality issues affect competing origins like West Africa and Pakistan. This steady external demand is a major factor in why prices are “holding” rather than correcting lower, even during peak harvest times when prices might typically dip.

Future Outlook and Strategic Advice

The report concludes with a neutral to mildly bullish outlook for the next two to four weeks. While the market is currently range-bound, the combination of potential weather damage in Thailand and a possible tightening of logistics in Vietnam suggests that the downside for prices is limited. Industry experts suggest that buyers consider securing coverage for the third and fourth quarters of 2026 now to hedge against potential price spikes if fresh market volatility eventually spills over into the processed segment.